Materiality – What we address in the Report

The Bank identifies material aspects which impact the Bank and its stakeholders on a priority basis, with a practical approach to integrated value creation.

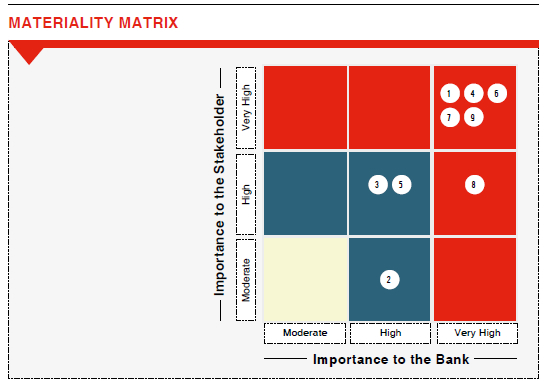

It is not practicable to address all possible issues that may have a bearing, on the Bank’s activities. We therefore address only the aspects that are material. An aspect is deemed to be material if it substantively affects the Bank’s ability to create value over the short, medium and long-term. Relevance and significance thus determine materiality, while taking significant account of both the magnitude of the impact as well as its probability of occurrence. An aspect can be important from two different perspectives, namely, that of the Bank and its stakeholders. Through an effective stakeholder engagement process we identify the topics material to the Bank. This is depicted through a two-dimensional materiality matrix shown below:

Due to the materiality assessment done by the Bank, there are some changes in Material topics from the previous year.

All the Material Aspects are identified in the process for defining report content.

| Topics |

Topic – Specific Disclosure |

The Importance to Bank |

The Importance to Stakeholders |

| Economic |

|

|

|

| 1. |

Economic Performance |

201-1 |

Very High |

Very High |

| |

|

201-3 |

Very High |

Very High |

| 2. |

Market Presence |

202-2 |

High |

Moderate |

| Environmental |

|

|

|

| 3. |

Energy |

302-1 |

High |

High |

| Social |

|

|

|

| 4. |

Employment |

401-1 |

Very High |

Very High |

| |

|

401-2 |

Very High |

Very High |

| |

|

401-3 |

Very High |

Moderate |

| 5. |

Labour/Management Relations |

402-1 |

High |

High |

| 6. |

Training and Education |

404-1 |

Very High |

Very High |

| |

|

404-2 |

Very High |

Very High |

| |

|

404-3 |

High |

Very High |

| 7. |

Diversity and Equal Opportunity |

405-1 |

High |

High |

| |

|

405-2 |

Very High |

Very High |

| 8. |

Marketing and Labelling |

417-1 |

Very High |

High |

| 9. |

Customer Privacy |

418-1 |

Very High |

Very High |